Read This Before You Sell Anything Online

First, let's start with a traditional counter sale. Think of this as a purchase at the hardware store or the local grocery store. You walk up to the counter with your stuff, the clerk rings it up and you pay with cash, check or a credit card. If you use the last option, you'll probably have a credit card machine in front of you that can be used to swipe or insert your card. This is referred to in the banking industry as a "retail transaction" or a "card present" transaction because your credit card is present and visible for inspection against fraud.

Now that you understand the basic "card present" model, let's move on to everything else, which is where most of you reading this will fit. If you aren't using a counter sale device like the one mentioned in the previous paragraph, then you fit into the "e-commerce" category. This is basically any transaction that is made in a way other than a retail sale. With all the fantastic technology available today, this can include restaurant sales at the table with a device like an iPad or a sale at a food truck, trade show, or web site. It also includes transportation sales like taxis, Lyft and Uber. All these non-retail or e-commerce sales have one thing in common - they require the Internet in order to transmit the payment details.

Transactions that happen over the Internet use something called a gateway. The gateway's job is to securely transmit the payment information from your Internet connected device to the credit card processor. It requires connections and conversations with multiple parties including your card processor, the customer's card company and your point of sale device. This all happens in less than 5 seconds and results in either an approval or a decline. Website shopping carts, smart phones, laptops, tablets, smart watches and automated phone payment systems all use a gateway. Amazon is the largest example of the gateway transaction process.

If you are considering how to sell your "things" online then you've no doubt seen the multitude of options available. Many companies will try to sell you on a "one step" sale process. They never mention the actual pieces or components involved. In short, they don't talk about gateways. Square and Paypal are examples. They have their own gateway and integrate it so tightly that the customer never sees under the hood. There is a downside to this type of product though. It's considerably more expensive. That extra 0.25% may not seem like a lot to you, but I encourage you to multiply your annual sales by 0.25%. Now do you see my point? These types of products are typically super simple to use but they are very limited in scale, meaning your business will probably outgrow them (and realize the need to stop wasting profit margin) quickly.

For a better option, consider a gateway product like Authorize.net. It is literally the worlds largest gateway in terms of customer use. They also have some of the best customer support on the planet (something Paypal is NOT known for). They also work with almost everything out there, from software payment platforms like storage company management software (monthly billing anyone?) to bowling alleys and healthcare billing.

If you need help navigating options, reach out to us. We'll be glad to help. If you're looking for a great price on an Authorize.net gateway or card processing, we can help with that also.

Best of success to you.

What is your real rate to take credit cards?

But that’s not your REAL rate. At least, not most of the time.

Well then, how do you figure out your REAL rate? The simplest method is to take all of your card transactions of the same type (ie. all Visa cards) and divide the total of all fees by the total dollar amount processed. This will give you the actual rate you’re paying to take Visa. It’s technically an average, but closer to reality than what you were quoted by your merchant processor.

Is it really more expensive to take American Express?

American Express cards are ALWAYS charged the same rate. All of them. Every time. Yes, they are a slightly higher rate. The key word being slightly. When you consider the previous factors, the gap is not as large as you think.

Is there any way to get a lower rate on Amex?

American Express intentionally prices their card rate at the top. One reason is because they know their customers are more valuable. Not everyone can get an American Express card, but almost anyone can get some sort of Visa card. Especially when you consider all the debit cards branded with MasterCard and Visa. If you refuse to take American Express, you are pissing off the elite group - you know, the ones with money that can actually afford to come back. This may not be a factor for your business. For example, if you sell water in the desert and you’re the only store in a 500 mile radius. If, on the other hand you sell something that has a higher level of competition, keep in mind that your customers have options. You may get them to pull out a different card THIS TIME, but there’s a pretty good chance they’ll remember that you don’t accept American Express when they think about coming back. That said, the good news is that American Express started offering interchange rates late in 2014, so there is SOME margin for negotiation. Just remember to factor in the “value” of the Amex cardholder when considering your merchant processing option.

As always, we are grateful for your business and appreciate the opportunity to be a trusted business partner.

If you need help, or you're looking for advice, give us a call.

A Successful Strategy to Grow Your Business that's Practically Free

One of the biggest challenges any business faces with regard to marketing, is the ability to reach a qualified audience. In layman’s terms, this means you want to advertise to people that have a high potential of buying your product. For example, if you sell parts for Ford Trucks, advertising to Chevy, Toyota, Nissan, etc owners is wasted effort, which translates to wasted advertising dollars. This is the reason billboards, television, radio and print advertising have declined. Simply hoping your demographic notices the advertisement, and happens to be someone that wants your product or service is not a great plan.

For these reasons, there is no better option on which to spend your advertising and marketing efforts than re-marketing. The return on your investment to focused re-marketing exceeds all other types of advertising many times over. In most cases, re-marketing is free or extremely inexpensive. As an added bonus, you can actually track this type of advertising to see what works, and with whom. If you have any interest in growing your business, you should be using re-marketing. Expecting growth without doing so equates to growing plants without water.

Would you be willing to offer a 5 or 10% discount if you had a guaranteed sale over and above any normal sales activity?

Consider this. If you’ve been in business for any amount of time, you already have a great opportunity to grow. The people that have been your customers in the past are a perfect match. They’ve shown enough interest to buy once, why not offer them an incentive to buy again? Discounts coupons, customer appreciation days, private sales for existing clients and advertising based on things from previous purchases are perfect examples of ways to re-market. The best part about all of this is that you don’t spend any funds out of your operating budget for this kind of advertising. It only costs you a discounted margin and only if the customer returns to buy again.

It’s absolutely mind numbing to me that more businesses don’t use this strategy.

Slowly, companies are catching on. This is why you see grocery stores offer you coupons that magically seem to be related to your previous purchases. They only print coupons that match your buying habits, and usually for things you haven’t bought lately.

There are quite a few software products that can help with customer management and purchase history. Many also have the ability to manage incentives, discount codes and loyalty programs. Each one is a little different, depending on the type of business you run.

As, with any attempts at business growth, YOU must take the first step. This usually starts with a plan or a definition of what outcome you seek. We can help with strategies and the best part - we don't charge for consultations. Get in touch if you'd like some guidance. We'd love to hear from you.

As always, we are grateful for your business and appreciate the opportunity to be a trusted business partner.

Best of success to you this month,

Keith

Is Expecting Your Digital Privacy Realistic?

Just about the only “positive” story on information privacy recently has come from Apple. Unfortunately, it has created a stir that has some negative views.

Most people don’t realize or value the extreme importance of protecting sensitive information. The reason can usually be traced back to one simple truth: identity theft has never happened to them. It is extremely flawed logic to think that because you’ve never experienced the negative consequences of data theft, it’s no big deal. Yet, here we are in a world where companies are repeatedly warned and then months later get caught with their pants down. Ask Target if they could have spent the $252 million on better things. Ask Home Depot how their attitude toward security is different now that they’ve spent $33 million on it. Do you think Hollywood Presbyterian Medical Center would invest in better security if they could go back in time?

Why don’t they take it more seriously? In addition to the “it won’t happen to me,” frame of mind, there is another prevailing factor. It can be expensive to secure and protect information. Hiring experts to manage data security, investing in network security equipment and maintaining security policies not only adds to the work load of everyone in the company, it also requires a dedicated budget. All of this for something that’s seen by decision makers and accountants as “not producing income.” The returns on this kind of investment are perceived as extremely nominal. This is especially the case for small business owners who frequently have neither the time, resources nor funding to establish the proper security. In my business, I see this this mindset every day. It’s more often the norm, which should scare the Hell out of everyone reading this.

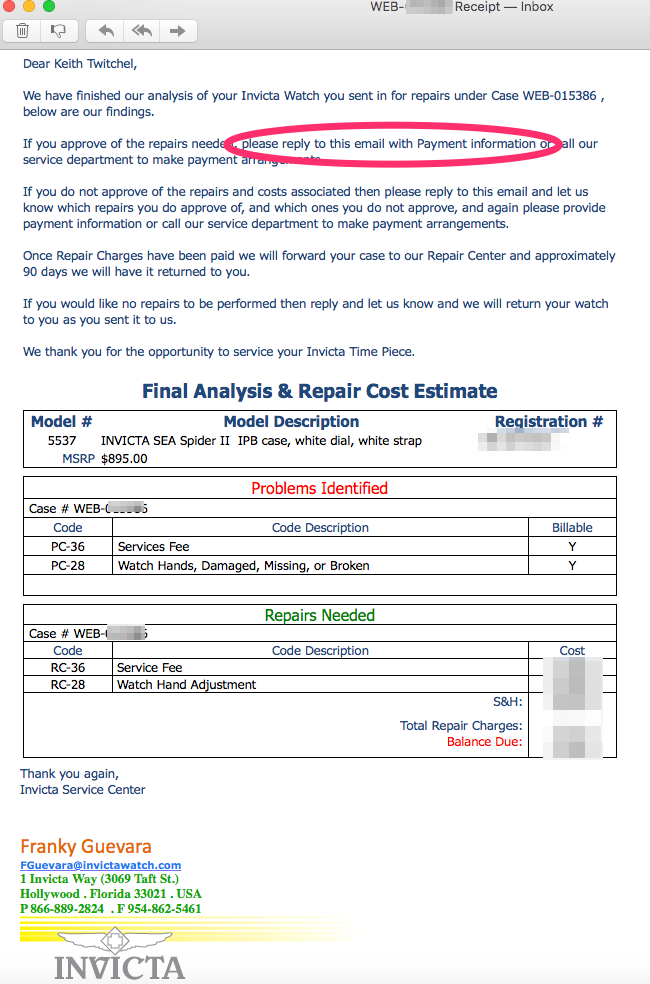

Don’t believe me? In the past month, I sent a wristwatch off for repair to the Invicta Watch Company. I received a form email from them asking me to respond with my credit card information. Later in the month, a support representative from Yabdab (a web software company) asked me to email administrator credentials for a server. It’s 2016. Do we really have explain to people that email is NOT secure?

{kind=link}

Unfortunately, the sobering truth is that until more people are affected and more companies are faced with negative consequences, your information is probably exposed somewhere right now.

What can you do? First, if you are a decision maker in your company, take steps to protect sensitive information that your customers have entrusted you with. Just like Uncle Ben said to Peter Parker, “With great power, comes great responsibility.” Second, be mindful of what you give out and to whom. If it doesn’t feel right, don’t do it. Ask if there’s another way. There usually is, but it requires extra effort. That effort will go a long way toward your privacy. Third, don’t allow companies to store your information when they ask. Yes, you will have to enter it every time, but is it REALLY so hard to do that? Don’t take shortcuts. Nothing is going to guarantee 100% protection of your information but you can increase the odds greatly if you try.

My company can provide more help with security. Especially in the area of PCI compliance. If you need assistance, we’d love to hear from you.

Thank You

The Alan Group has a reputation in the financial industry of being THE technical expert resource to help bankers and merchants solve challenges. In 20 years of business, we have never charged for consultations or for expert advice. Our goal is to make you successful. Many of you are not aware of this resource. For this reason, I'm creating a regular email message. It will be very infrequent. Roughly one per month. If I can help even a small group of you to grow through my strategies for best practices or ways to improve your methods, it’s worth it.

Getting paid on the go

This month’s expert advice comes in the form of a tip. Did you know that you can process payments on your mobile device (iPhone, iPad, Android) with an Authorize.net account? Most of you already have an Authorize.net account, and if you do, there’s absolutely no extra charge to use the mobile app to process payments. It’s already included with your account. If your business or charity collects payments at public events or trade shows, this is a great way to handle payments quickly. You can even send email receipts to your customers during checkout. The full instructions for setting up the Authorize.net mobile app can be found here for iOS: http://www.authorize.net/support/iosuserguide.pdf and here for Android: http://www.authorize.net/support/androiduserguide.pdf

Of course, you’re welcome to call or email us if you need a mobile card reader or just need help.

Thank you for allowing us to serve you in 2015. If you have questions, need help with your credit card or electronic check processing, web shopping cart or point of sale system you are welcome to call or email any time.

I wish the best of success to you in 2016.

-Keith